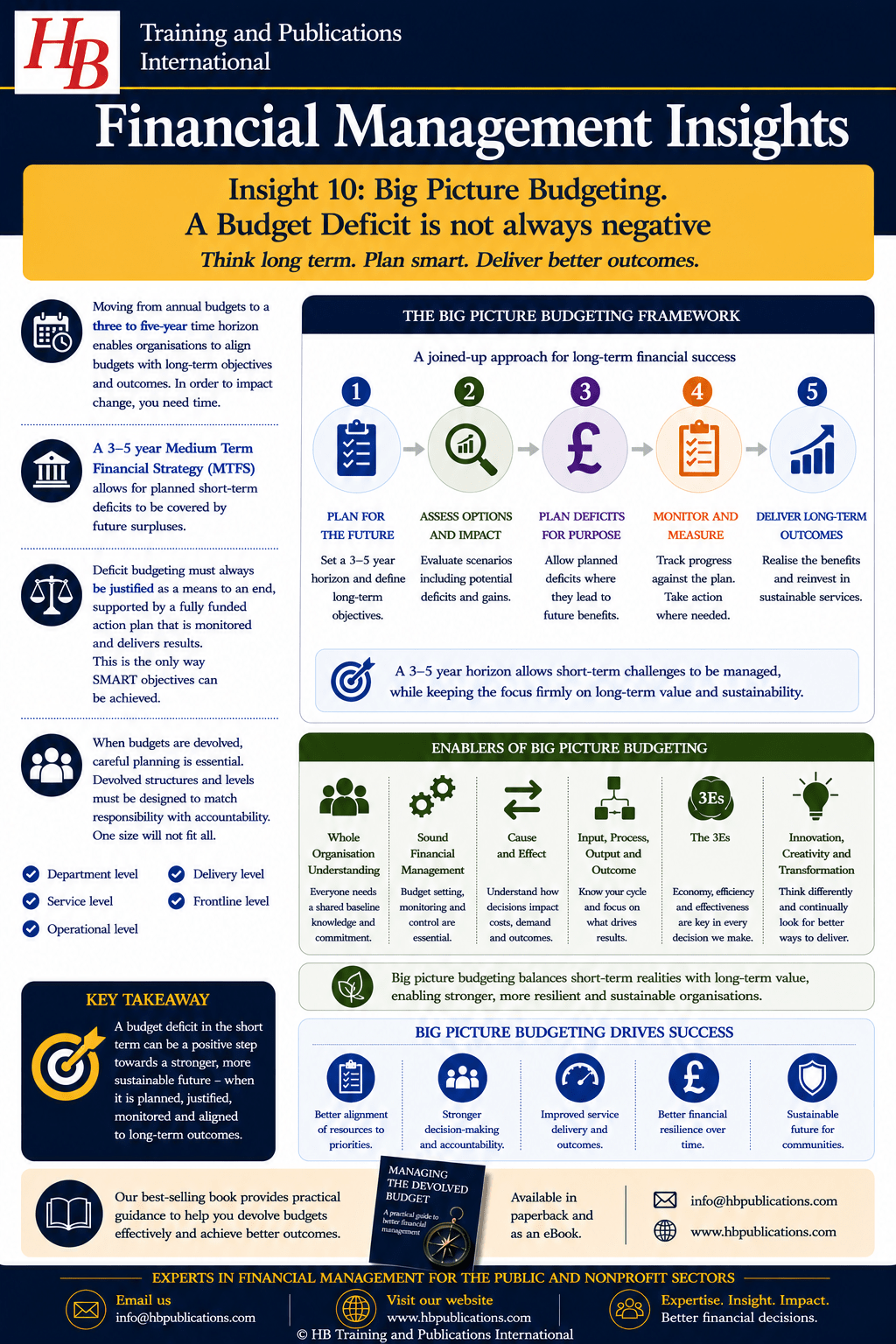

To move from annual budgets to a three to five-year time horizon for the public sector enables budgets to align with the big picture of long-term objectives and outcomes. In order to impact change, you need time.

The budgeting process, particularly in local government, has been focussed on an annual balanced budget which can be difficult to achieve. However, having a budget that reflects a 3-to-5-year Medium Term Financial Strategy (MTFS) will allow for some years to have planned deficits knowing that these will be covered in future years.

There is a caveat however, deficit budgeting must always be justified as a means to an end, and those preparing budgets must be confident in their ability to be realistic about the future. They must be sure that short term deficits lead to longer term gains through a fully funded action plan that can be monitored and yield results. This is the only way SMART objectives can be achieved.

The greater the level of devolved budgeting, the more care needs to be taken in the planning stages. Firstly, the devolved structure needs to be designed, including the level of devolvement which should be matched with accountability. For example – department level, service level, operational level, delivery level, frontline level. One size will not fit all. Levels of devolvement will differ and should be appropriate to the organisational objectives in each case.

Those with budget responsibilities will then need to create their plan for the time horizon, and ensure their big picture combines seamlessly within an overall framework and strategic plan for the organisation. This then allows for deficit budgeting in some areas, and surplus budgeting in others. This approach can only work if the whole organisation has a baseline understanding of budget setting, monitoring and control; impact of supply and demand; relationship between cause and effect; and a concrete knowledge of the input, process, output, and outcome cycle in their orbit of responsibility. Of course, everyone should be mindful of the 3Es whilst driving for innovation, creativity and transformation.

If you are finding our insights useful and wish to have more information, please get in touch at info@hbpublications.com or visit www.hbpublications.com

Our book – Managing the Devolved Budget – is available in paperback and as an eBook.

HB Training and Publications International: Experts in Financial Management in the public and nonprofit sectors